At MBE Wealth, we understand that market shifts—whether driven by economic policy, geopolitical events, or evolving investor sentiment—require a steady, informed approach. As we step into 2025, we remain committed to helping our clients navigate financial uncertainty with disciplined, research-driven investment strategies. The latest market movements, from tariff discussions to Federal Reserve decisions, highlight the importance of long-term planning and diversified portfolios. In this month’s market recap, we break down the key factors shaping the financial landscape and what they mean for investors moving forward.

Market Recap

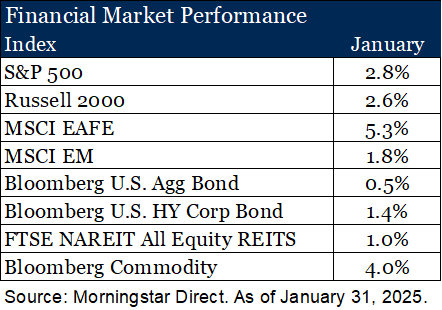

The start of the year marks both symbolic and literal new beginnings. President Trump took office on January 20, swiftly issuing a flurry of executive orders that kept investors scrambling to assess their implications. The notable absence of tariffs—our deep dive topic for the month—helped propel international markets higher. Markets, as forward-looking discounting mechanisms, had already priced in much of the tariff-related rhetoric during the fourth quarter. The absence of new developments acted as a relief valve for investors with acute concerns.

Another key driver of U.S. versus international market performance in January was NVIDIA. Shares of NVIDIA fell nearly 17% on January 27, accounting for 79% of the S&P 500’s one-day decline (-1.15% of the index’s -1.45% drop)[1]. The sell-off was triggered by news that Chinese startup DeepSeek had developed an AI model with quality comparable to U.S. models but with significantly lower capital investment and reduced need for advanced computing power—an implicit challenge to demand for NVIDIA products. For years, investors have grown accustomed to market concentration fueling U.S. equity returns. However, as we highlighted in our investment research partner, Fiducient Advisors' annual outlook, concentration also carries risks. Whether DeepSeek represents a "Minsky moment" for AI is beyond our remit, but this episode underscores the theme of fragility we noted in our outlook.

On the economic front, the Federal Reserve left interest rates unchanged in January and notably removed its standard language on improving inflation dynamics. With unemployment hovering around 4% and fourth quarter of 2024 GDP reported in January at 2.3%[2], the economy has little slack to absorb pro-growth policies without adding inflationary pressures. As a result, the Fed lacks both the motivation (a weakening economy) and the visibility (policy clarity) to pursue further easing at this time.

Historical Fed minutes—released with a five-year lag—reveal that policymakers in 2018 and 2019 prospectively discussed the economic impact of the Trump tariff policies when considering monetary policy. This latest decision aligns with our view that inflation risks remain elevated, reinforcing our portfolio positioning for 2025 and beyond.

Tariff Talk

Although tariffs were absent from the flurry of executive orders in January, February brought new developments, with Canada, Mexico, and China now in the spotlight. While the situation remains fluid, we’ll take this as an opportunity to put tariffs into context and examine their potential impact.

A Historical Perspective

President Trump is not pioneering new territory here. While modern tariffs, including those implemented in 2018 and 2020, have played a modest role in economic policy, tariffs have had a more prominent role historically. In the past, they have been used to attempt economic fairness (with “fairness” being subject to interpretation), protect domestic industries, and generate government revenue.

Recent tariff supporters who face criticism of inflation often dust off history books and point to the Smoot-Hawley Tariffs of the 1930s as evidence that tariffs alone are not inflationary. It is true that the taxation of over 20,000 goods—leading to an effective tariff of ~20%—coincided with flat or even moderating CPI levels[3]. But let’s not forget the broader economic backdrop: the U.S. was in the depths of the Great Depression, with the economy contracting sharply. Hardly the definitive proof one might hope for.

Fast forward to modern times. The tariffs imposed during Trump’s first administration in 2018 and expanded by President Biden in 2020 coincided with inflation surging from multi-decade averages of ~3% to over 9% by 2022[4]. Other prevailing economic factors were also at play during that period. The government responded to the COVID-19 pandemic by dramatically expanding the money supply, keeping interest rates at historic lows, continuing quantitative easing until March 2022, rolling out massive fiscal stimulus, and running up deficit spending (which continues today). Tariffs were just one piece of a much larger inflationary puzzle.

The Economic Punchline

Basic economic principles suggest tariffs are inherently inflationary. Why? Even without retaliatory tariffs—which we think are likely—companies facing higher input costs will pass those increases on to consumers. That translates to higher prices and, in effect, is policy-manufactured inflation. However, the actual inflationary impact depends on broader economic conditions, as demonstrated by history.

What This Means for 2025

- Tariffs Raise Inflation Risks—But Aren’t the Only Factor - As Fiducient Advisors outlined in their 2025 Outlook – Bridging the Divide, the risk of accelerating inflation has increased for numerous reasons. If tariffs are enacted, the extent and scope will likely add upward pressure on prices. However, they won’t be the sole driver of inflation.

- Tariff Impacts Tend to Be Temporary, Not Structural – Just as tariffs can be imposed quickly, they can be reversed just as fast. Long-term investors are likely to see greater success by focusing on fundamental drivers—valuations, earnings growth, and diversification, to name a few—rather than short-term policy moves.

- Expect Noise – Tariffs are often used as a bargaining tool rather than purely an economic policy. Take Colombia, for example. In a recent headline-grabbing episode, the new administration sought to deport migrants back to their home country. When Colombia initially resisted, a brief standoff ensued, involving tariff threats. After a few deportation flights landed, the tariff threats disappeared. The new administration has shown far greater willingness to use these tactics than in the recent past. We expect more of these episodes, which could create short-term market volatility. For long-term investors, such moments often present opportunities rather than fundamental shifts.

Looking Ahead

The start of the year has offered many opportunities to shift our investment focus from the long-term to the short-term, reacting to market fluctuations and headlines. However, our investment strategy remains the same—looking beyond headline-driven noise to allocate capital where we see the most compelling long-term returns.

As markets continue to evolve, staying informed and making well-planned financial decisions is more important than ever. At MBE Wealth, we are committed to providing insights and strategies to help you navigate these changes with confidence. Whether you're reviewing your investment approach or planning for the future, our team is here to support your financial goals. Connect with us today to discuss how we can help—visit MBE Wealth to get started.

Disclosures

Sources

[1] Morningstar as of January 29, 2025

[2] Bureau of Economic Analysis Advanced Estimate of 4Q GDP as of January 30, 2025

[3] The Peterson Institute as of December 31, 2024

[4] Bureau of Labor Statistics Consumer Price Index as of January 15, 2025

Definitions

Comparisons to any indices referenced herein are for illustrative purposes only and are not meant to imply that actual returns or volatility will be similar to the indices. Indices cannot be invested in directly. Unmanaged index returns assume reinvestment of any and all distributions and do not reflect our fees or expenses.

- The S&P 500 is a capitalization-weighted index designed to measure the performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

- Russell 2000 consists of the 2,000 smallest U.S. companies in the Russell 3000 index.

- MSCI EAFE is an equity index that captures large and mid-cap representation across Developed Markets countries around the world, excluding the U.S. and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

- MSCI Emerging Markets captures large and mid-cap representation across Emerging Markets countries. The index covers approximately 85% of the free-float adjusted market capitalization in each country.

- Bloomberg U.S. Aggregate Index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

- Bloomberg U.S. Corporate High Yield Index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included.

- FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property.

- Bloomberg Commodity Index is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually, weighted 2/3 by trading volume and 1/3 by world production, and weight-caps are applied at the commodity, sector, and group levels for diversification.

Material Risks

- Fixed-income securities are subject to interest rate risks, the risk of default, and liquidity risks. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations.

- Cash may be subject to the loss of principal and, over longer periods of time may lose purchasing power due to inflation.

- Domestic Equity can be volatile. The rise or fall in prices takes place for a number of reasons, including, but not limited to, changes to underlying company conditions, sector or industry factors, or other macro events. These may happen quickly and unpredictably.

- International Equity can be volatile. The rise or fall in prices takes place for a number of reasons, including, but not limited to, changes to underlying company conditions, sector or industry impacts, or other macro events. These may happen quickly and unpredictably. International equity allocations may also be impacted by currency and/or country-specific risks, which may result in lower liquidity in some markets.

- Real Assets can be volatile and may include asset segments that may have greater volatility than investments in traditional equity securities. Such volatility could be influenced by a myriad of factors including, but not limited to, overall market volatility, changes in interest rates, political and regulatory developments, or other exogenous events like weather or natural disasters.

- Private Real Estate involves higher risk and is suitable only for sophisticated investors. Real estate assets can be volatile and may include unique risks to the asset class, like leverage and/or industry, sector, or geographical concentration. Declines in real estate value may take place for a number of reasons, including, but not limited to, economic conditions, changes in the condition of the underlying property, or defaults by the borrower.